Most contractors assume that if a subcontractor walks off a job or goes under mid-project, a surety bond or standard liability policy will cover the fallout. That assumption can be dangerously expensive. Subcontractor default insurance (SDI) is a specialized, first-party insurance product that fills a very specific gap in project risk management, and most trade professionals in the US, UK, and Australia have never had it properly explained to them. This guide breaks down exactly what SDI is, how claims work, how it compares to other risk tools, and what regional differences you need to know before relying on it.

Table of Contents

- Understanding subcontractor default insurance

- How SDI claims work: Triggers, process, and limitations

- SDI versus surety bonds and other insurance: Key differences

- International context: SDI in the US, UK, and Australia

- Our experience: The truths and traps of SDI for contractors

- Get support with SDI and project risk management

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| SDI protects general contractors | Subcontractor default insurance reimburses the general contractor if a subcontractor fails to perform, covering direct project losses. |

| Claiming requires documentation | GCs must document the default and provide detailed evidence and timely notice to activate SDI coverage. |

| Not a substitute for all insurance | SDI does not replace the need for subcontractor liability insurance or guarantee coverage for every loss. |

| Regional differences matter | SDI is most common in the US; UK and Australian markets often use alternative security or insurance mechanisms. |

| Beware of retention and exclusions | Large deductibles, co-pays, and policy exclusions mean SDI is only part of a comprehensive risk strategy. |

Understanding subcontractor default insurance

SDI is not a catch-all policy. It has a precise purpose, a specific buyer, and a defined trigger. Getting those details wrong can leave a general contractor (GC) exposed at exactly the wrong moment.

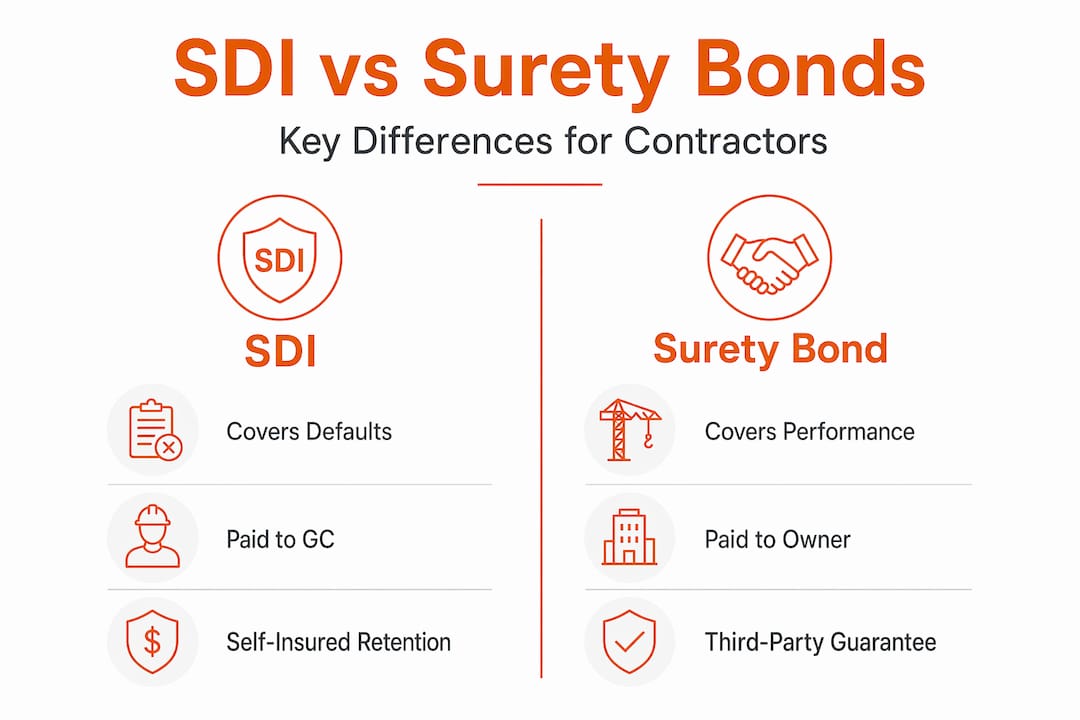

As a starting point, SDI is a construction risk-management insurance product where the general contractor (policyholder) buys coverage to be reimbursed if an enrolled subcontractor fails to perform, meaning they default. The GC pays the premiums, the GC files the claim, and the GC receives the payout. The subcontractor is not a party to the policy at all.

This is a critical structural distinction. SDI is typically structured as first-party insurance held and administered by the general contractor, not a three-party performance guarantee like a surety bond. That difference changes everything about how fast you can respond to a default and how much control you retain during the recovery process.

Here is a quick breakdown of the core features:

- Who holds the policy: The general contractor, not the subcontractor

- Claim triggers: A subcontractor's failure to perform, abandonment, insolvency, or material breach of contract

- What costs are covered: Completion costs, re-procurement expenses, delay-related costs, and sometimes legal fees tied to the default

- Difference from surety bonds: SDI is a direct insurance reimbursement; a surety bond is a three-party guarantee where the surety investigates and controls the response

| Feature | SDI | Surety bond |

|---|---|---|

| Who buys it | General contractor | Subcontractor (for the GC's benefit) |

| Who controls the response | GC | Surety company |

| Speed of response | Faster, GC-driven | Slower, surety-driven |

| Cost structure | Premium plus retention/co-pay | Bond premium (typically 1-3% of contract value) |

| Flexibility | High, GC chooses replacement | Lower, surety may dictate options |

| Coverage scope | Broad default costs | Performance and payment obligations |

"SDI's greatest advantage is speed. When a subcontractor defaults on a critical-path trade, waiting for a surety to investigate and authorize action can cost more than the default itself. SDI lets the GC act immediately and seek reimbursement after the fact." — Construction risk management consultant

That speed is not a minor convenience. On a large commercial project, every day of delay on a critical trade can generate tens of thousands of dollars in cascading costs. SDI is specifically designed to keep the project moving while the financial recovery happens in parallel.

How SDI claims work: Triggers, process, and limitations

Now that the basics are clear, the next thing to understand is what happens when a subcontractor default actually occurs. The claims process is more involved than most GCs expect, and the documentation requirements are strict.

Here is a step-by-step look at how a typical SDI claim unfolds:

- Identify the default: The GC recognizes that a subcontractor has failed to perform, abandoned the project, or become insolvent. The trigger must match the policy's defined default events.

- Issue formal notice: The GC provides written notice to the subcontractor and notifies the insurer within the timeframe specified in the policy. Missing this window can void the claim.

- Document everything: Daily logs, photos, correspondence, and financial records must be gathered immediately. Gaps in documentation are one of the top reasons claims are reduced or denied.

- Mitigate the loss: The GC must take reasonable steps to minimize costs, including re-procuring a replacement subcontractor promptly. Failure to mitigate can reduce the claim payout.

- Submit the claim: The GC submits all documented costs, including completion contracts, labor overruns, and delay costs, to the insurer for review.

- Receive reimbursement: After the insurer reviews and approves the claim, the GC is reimbursed for covered costs above the retention layer.

SDI claims involve documenting the subcontractor default, and policy terms often govern notice timing, evidence and mitigation documentation, and what costs are eligible. This is not a policy you can manage casually.

One of the most surprising aspects of SDI for first-time buyers is the self-insured retention (SIR), which is essentially a large deductible. SIRs on SDI policies commonly range from several hundred thousand dollars to low millions, depending on the GC's size and the policy structure. On top of that, most SDI policies include a co-insurance or co-pay requirement, typically between 10% and 20% of covered losses. That means even after the SIR is met, the GC absorbs a portion of every dollar claimed.

Pro Tip: Treat your SDI policy as a complement to rigorous subcontractor prequalification, not a substitute for it. The best SDI outcome is one you never need to trigger. Maintain detailed daily site logs, require subcontractors to submit regular progress reports, and document any warning signs of financial distress early.

It is also worth being clear about what SDI does not cover. Common exclusions include:

- Subcontractors not formally enrolled in the policy before the default

- Losses caused by the GC's own actions or negligence

- Consequential damages not directly tied to the default event

- Trades or contract values that exceed per-trade or per-project caps in the policy

- Defect claims that arise after project completion rather than during performance

Understanding these exclusions before you need to file a claim is the difference between a covered loss and an out-of-pocket disaster.

SDI versus surety bonds and other insurance: Key differences

Understanding the SDI claim process brings up an important question: how is SDI different from other familiar project risk tools? The comparison matters because GCs sometimes treat SDI as a wholesale replacement for bonds or other coverages, which creates real gaps.

SDI can be used as an alternative to surety bonds for subcontractor performance risk, but it generally does not replace other required contractor and subcontractor insurance obligations. That is a crucial line to hold.

| Risk tool | Protects | Controlled by | Best for |

|---|---|---|---|

| SDI | GC's project completion costs | GC | Large projects with multiple enrolled subs |

| Surety bond | GC and owner | Surety company | Projects requiring third-party guarantee |

| Sub liability insurance | Third parties injured by sub's work | Subcontractor | Ongoing liability from sub's operations |

| Builder's risk insurance | Physical property during construction | Policy holder (GC or owner) | Damage to the structure itself |

Pros of SDI for GCs:

- Faster response and greater control during a default event

- Can cover a portfolio of subcontractors under one policy

- Potentially lower cost than requiring bonds from every subcontractor

- Covers a broader range of default-related costs than most surety bonds

Cons of SDI for GCs:

- Large SIR means the GC absorbs significant first-dollar losses

- Requires robust internal prequalification and documentation systems

- Enrollment rules mean not every sub is automatically covered

- Premium costs can be significant on large programs

From the subcontractor's perspective:

- SDI does not protect you. It protects the GC from your default.

- You still need your own general liability, workers' compensation, and professional indemnity coverage.

- Being enrolled in a GC's SDI program is not a substitute for your own insurance obligations.

"SDI is a GC-side risk management tool. Subcontractors who assume their enrollment in a GC's SDI program provides them any coverage are operating under a serious misconception. Their own insurance program must remain intact and current regardless of any SDI arrangement." — Construction insurance specialist

In the US, SDI has become a well-established tool for large GCs managing complex, multi-trade projects. The product is widely available through specialty insurers and has a track record of supporting rapid project recovery after defaults on commercial and infrastructure work.

International context: SDI in the US, UK, and Australia

Having compared SDI and related products, it is crucial to recognize how region affects risk coverage options and obligations. SDI is not a globally uniform product, and what works in the US may not be directly available or legally recognized in the UK or Australia.

United States: SDI is a mature, well-understood product in the US construction market. Major specialty insurers offer SDI programs, and many large GCs use SDI as their primary tool for managing subcontractor performance risk on projects above a certain dollar threshold. The product is particularly common on commercial, industrial, and infrastructure projects where multiple specialty trades are enrolled under a single GC-held policy.

United Kingdom: The UK construction market does not have a standardized SDI equivalent. Risk management for subcontractor default in the UK tends to rely on contractual protections, retention clauses, and performance bonds under standard forms like JCT or NEC contracts. Insolvency risk is typically managed through contract terms and, in some cases, specialist credit or insolvency insurance products rather than a GC-held SDI policy.

Australia: UK and Australia context: sources emphasize other security and insolvency protections and retention insurance rather than a standardized SDI equivalent. In Australia, the focus has been on statutory insurance schemes, particularly in the residential sector, and on retention trust arrangements rather than a GC-purchased default insurance product. Builders and contractors in Australia should look to domestic insolvency protections, project bank accounts, and retention trust legislation in their specific state or territory.

Regional differences to keep in mind:

- US: SDI is widely available and commonly used on commercial projects above $10 million

- UK: Performance bonds and contractual retention are the primary tools; no direct SDI market

- Australia: State-based insolvency insurance schemes and retention trusts are the dominant protective mechanisms; SDI is not a standard product

- All regions: Subcontractors must maintain their own liability and workers' compensation coverage regardless of what the GC holds

- All regions: Always verify what is required or accepted by the project owner, lender, or relevant authority before selecting a risk tool

The practical takeaway here is straightforward. If you are a GC or subcontractor operating in the UK or Australia, do not assume that SDI-style coverage is available or appropriate for your project. Work with a local construction insurance specialist to identify the right combination of bonds, insurance, and contractual protections for your jurisdiction.

Our experience: The truths and traps of SDI for contractors

With the technical facts in mind, here is a hard-won perspective on what actually works when using SDI on real projects, and where contractors consistently get burned.

The single biggest surprise for GCs entering an SDI program for the first time is the size of the retention layer. SDI structures often include large retentions and co-pays, so SDI may not be a substitute for adequate balance-sheet capacity on the retention layer. A GC with a $500,000 SIR and a 15% co-pay on a $2 million default event is still absorbing $650,000 out of pocket before the policy meaningfully kicks in. That is not a small number for most regional contractors.

The second trap is enrollment complacency. GCs sometimes assume that all their subcontractors are automatically covered once they purchase an SDI policy. They are not. Each subcontractor must typically be prequalified and formally enrolled, and the insurer may reject certain trades, contract values, or subs with weak financials. If a non-enrolled sub defaults, the GC has no SDI coverage for that event, period.

Pro Tip: Always review your SDI policy's trade caps, per-sub limits, and enrollment rules at the start of every project. Build enrollment confirmation into your subcontract execution checklist so nothing slips through.

The third and most dangerous misconception is treating SDI as a risk elimination tool rather than a cash-flow management tool. SDI does not make the risk of subcontractor default disappear. It shifts the timing of the financial impact and reduces the ultimate out-of-pocket cost. The best risk management strategy still starts with rigorous prequalification, strong subcontract language, active performance monitoring, and a healthy balance sheet that can absorb the retention layer without destabilizing the business.

SDI is a powerful tool. But it works best for contractors who treat it as one layer in a broader risk management system, not as a standalone safety net.

Get support with SDI and project risk management

Managing SDI documentation, subcontractor enrollment, and project risk compliance is a significant operational challenge. The paperwork, daily logs, prequalification records, and financial tracking that SDI requires are exactly the kinds of tasks that can slip through the cracks on a busy job site.

Subascent's job and bid management software is built specifically for trade contractors and subcontractors in the US, UK, and Australia who need to keep their project records tight, their bids competitive, and their risk exposure visible. Whether you are a GC managing a portfolio of enrolled subs or a trade contractor trying to stay compliant with documentation requirements, Subascent gives you the digital infrastructure to stay organized and in control. Built on over 80 years of industry experience, the platform is designed for the practical realities of electrical, plumbing, HVAC, concrete, roofing, and other specialty trades. Explore how smarter project tracking can support your risk management from day one.

Frequently asked questions

Who actually benefits from subcontractor default insurance?

SDI is designed to protect the general contractor from the financial costs of a subcontractor failing to perform, and it does not provide any direct coverage to the subcontractor itself.

Does SDI replace the need for subcontractor liability insurance?

No. Subcontractors still need their own liability, workers' compensation, and other required insurance because SDI does not replace other required contractor and subcontractor insurance obligations.

Is there a standardized SDI product in the UK or Australia?

No. SDI as practiced in the US is not a standard product in the UK or Australia, where other insolvency protections and retention insurance mechanisms are more commonly used.

What is typically not covered by SDI?

SDI policies generally exclude costs for subcontractors not enrolled in the policy, losses caused by the GC's own actions, and trades or losses that fall outside the policy's enrollment rules or coverage caps.