A surety bond is a financial guarantee from a licensed surety company that your trade business will fulfill its contractual obligations on a construction project. For electrical, plumbing, HVAC, roofing, and masonry contractors, understanding how bonding works is the difference between qualifying for a project and being shut out of the bid. Bonding involves three parties: you as the principal, the project owner as the obligee, and the surety company backing your performance. Premiums typically run 1%–3% of contract value, and the underwriting process is more rigorous than any insurance application you have filled out.

How does the bonding process work for small contractors?

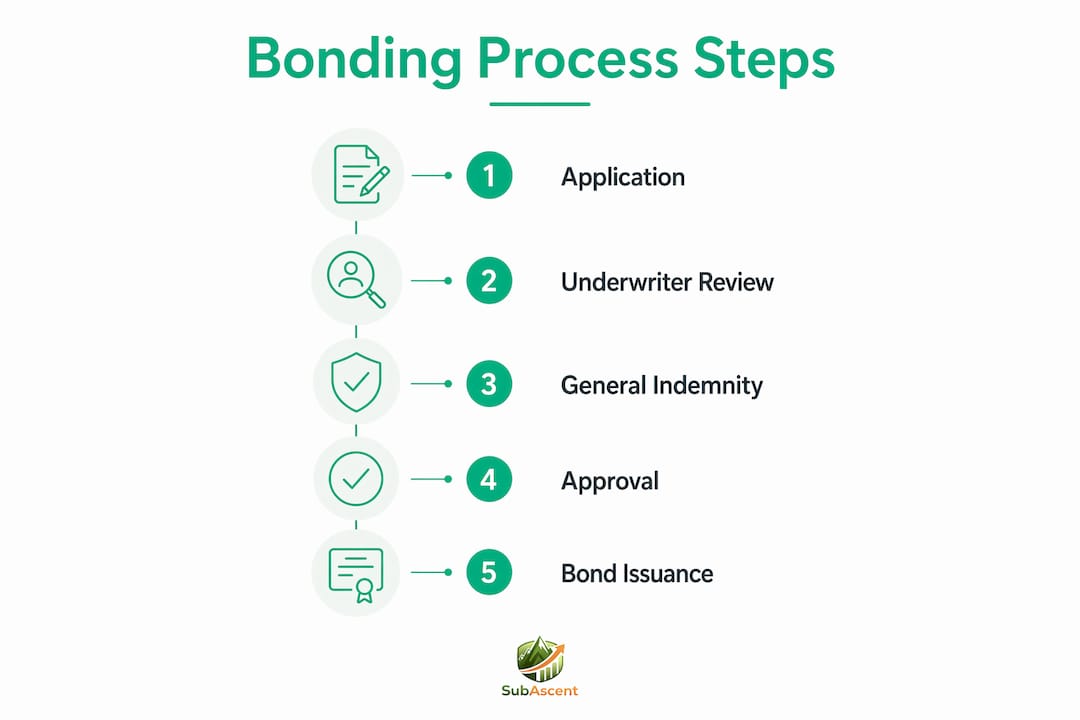

The bonding process for small contractors starts with a surety bond application submitted through a licensed broker. The surety company then underwrites your business the same way a bank underwrites a loan. They are not just checking a box. They are deciding whether your business is a credit risk.

The application requires financial and operational documentation. Expect to provide:

- Two to three years of business tax returns and financial statements

- A current balance sheet showing assets, liabilities, and working capital

- A work-in-progress (WIP) report showing active jobs and completion percentages

- Your personal financial statement and credit history

- A resume of completed projects with contract values and references

The underwriter evaluates three things: your financial strength, your experience in the type of work being bonded, and your capacity to take on additional work without overextending. A drywall contractor with five completed $800,000 projects and clean financials will get approved faster than one with one $2 million project and no track record.

You will also sign a General Indemnity Agreement (GIA). This is the document most contractors sign without reading carefully. The GIA makes you personally liable for any losses the surety pays out, including investigation costs and legal fees. Your personal assets are on the line, not just your business.

Turnaround times run from 24 hours for small bonds under $500,000 to two weeks or more for large or complex projects. Accurate, complete applications move faster. Missing documents are the single biggest cause of delays.

Pro Tip: Submit your financial statements prepared by a CPA, not just compiled internally. Surety underwriters weight CPA-reviewed or audited statements significantly higher than self-prepared documents.

What factors affect bonding costs and approval odds?

Bond premiums are calculated as a percentage of the total contract value. Established contractors pay 1%–3% of contract value in premiums. On a $500,000 roofing or fire protection contract, that means $5,000 to $15,000 in bond cost. That number matters when you are building your bid.

New contractors or those with credit issues pay 3% or higher. That higher rate reflects the surety's increased risk. It also compresses your margin if you are not accounting for it in your estimate.

Here is how approval odds break down by contractor profile:

- Established contractor, strong credit, clean financials. Approved at standard rates with minimal documentation requests. Fastest path to bonding.

- New contractor, limited project history. Higher premiums, smaller bond limits, and more documentation required. The SBA Surety Bond Guarantee Program is your best option here.

- Contractor with credit issues or prior claims. Hardest to bond through standard markets. SBA program or specialty surety markets are the primary options.

- Contractor with strong financials but large project jump. Likely declined if the jump is too large. Sureties prefer incremental growth of 20%–30% in project size, not a leap from $1 million to $5 million.

The SBA Surety Bond Guarantee Program is a real tool, not just a footnote. The SBA guarantees 80%–90% of surety losses on contracts up to $9 million for standard projects and $14 million for federal work. That guarantee lets sureties approve contractors they would otherwise decline. If you are a concrete or framing contractor trying to break into larger public work, this program is worth a direct conversation with a surety broker.

Working capital is the underlying driver of your bonding limit. The rule of thumb is working capital multiplied by 15–20 to estimate your total bonding capacity. A contractor with $200,000 in working capital can typically support $3 million to $4 million in bonded work. Retaining 50%–75% of net profits inside the business over three to five years is the most direct way to grow that number.

Pro Tip: Do not distribute all profits at year end. Retained earnings sitting inside your business increase your working capital and directly expand your bonding capacity. Talk to your CPA before making distributions.

How is bonding different from insurance?

Surety bonds and insurance look similar from the outside. Both involve a third party and a premium payment. The mechanics are completely different, and confusing them is a costly mistake.

Insurance is a two-party agreement. You pay a premium, the insurer accepts the risk, and if a covered loss occurs, the insurer pays without coming back to you for reimbursement. General liability, workers' comp, and builder's risk all work this way.

A surety bond is a three-party credit instrument. Consider these key distinctions:

- Who is protected. Insurance protects you, the contractor. A bond protects the project owner (obligee). You are not the beneficiary of your own bond.

- Who absorbs the loss. An insurer absorbs the loss. A surety does not. The surety expects zero loss and will pursue full reimbursement from you after paying a claim.

- Underwriting rigor. Insurance underwriting prices in expected losses. Surety underwriting assumes no losses will occur. That is why the surety digs so deep into your financials and project history.

- Personal liability. Insurance does not make you personally liable beyond your premium. The GIA on a bond does.

A surety bond is not a safety net for the contractor. It is a guarantee to the project owner that the contractor will perform. If the surety pays a claim, the contractor owes every dollar back.

This distinction matters for HVAC, low-voltage, and glazing contractors who are new to bonded work. You cannot treat a bond claim the way you treat an insurance claim. The financial exposure is personal and direct. For a deeper look at how bonds compare to other contractor protections, the Subascent guide on subcontractor default insurance covers the risk landscape clearly.

What practical steps improve bonding success and capacity?

Getting bonded is not a one-time transaction. It is an ongoing relationship with a surety company that grows as your business grows. These steps apply whether you are a painting contractor applying for your first bond or an insulation contractor trying to increase your single-project limit.

Work with a surety-specific broker. A general insurance agent is not the right partner here. Surety-specific brokers advocate for contractors by framing your financials in the way underwriters want to see them. They know which sureties are favorable to your trade and project type. That knowledge directly improves your approval odds and can reduce your premium rate.

Keep financial records current and detailed. Sureties want current data. A balance sheet from 14 months ago is a red flag. Maintain monthly financial statements, keep your WIP report updated, and have your CPA prepare year-end financials within 90 days of fiscal year close. A financial dashboard built for trade subs makes this significantly easier to maintain consistently.

Grow project size incrementally. A contractor completing five $1 million projects is typically approved for a $1.5 million project next. A jump to $5 million will likely be declined. Sureties read large jumps as a capacity risk, not ambition. Build your track record at each level before pushing higher.

Retain profits inside the business. Distributions reduce working capital. Working capital drives bonding capacity. If you pull out all profits each year, your bonding limit stays flat. Retaining 50%–75% of net profits over three to five years compounds your capacity significantly.

Here is a quick comparison of two approaches to bonding growth:

| Approach | Result |

|---|---|

| Distribute all profits annually | Working capital stays flat, bonding limit stagnates |

| Retain 50%–75% of net profits | Working capital grows, bonding capacity expands each year |

| Work with a general insurance agent | Slower approvals, higher premiums, weaker advocacy |

| Work with a surety-specific broker | Faster approvals, better rates, stronger underwriting presentation |

Submit bond applications separately from insurance renewals. Handling bonds independently speeds approvals and prevents delays in bidding. Also verify that the obligee name on your bond matches the contract documents exactly. Mismatches are a common rejection cause that costs you time on live bids.

Pro Tip: Before submitting any bond application, confirm the exact legal name of the obligee and the required bond form number. A mismatch between your bond and the contract document is an automatic rejection, even if everything else is correct.

For contractors getting into public work and competitive bidding, the Subascent overview of trade bidding requirements covers how bonding fits into the broader qualification process.

Key takeaways

Surety bonds are credit instruments that protect project owners, not contractors, and the contractor bears full personal liability for any surety losses through the General Indemnity Agreement.

| Point | Details |

|---|---|

| Bond premiums cost real money | Budget 1%–3% of contract value for established contractors; factor this into every bonded bid. |

| GIA creates personal liability | You owe the surety every dollar it pays on a claim, including legal and investigation costs. |

| SBA program opens doors | The SBA Surety Bond Guarantee Program covers up to 90% of losses, helping new or credit-challenged contractors qualify. |

| Working capital drives capacity | Multiply working capital by 15–20 to estimate your bonding limit; retain profits to grow it. |

| Grow project size incrementally | A 20%–30% increase in project size is the range sureties approve; large jumps get declined. |

Bonding is the financial test most trade contractors are not prepared for

I have watched solid trade contractors lose bids not because their price was wrong or their crew was weak, but because their bonding was not in order. An electrical contractor with 12 years of field experience and a clean safety record got shut out of a $2.5 million school project because his working capital was too thin and he had never built a relationship with a surety broker. He had the skills. He did not have the financial structure.

The contractors who navigate bonding well treat it the same way they treat their equipment. They maintain it, invest in it, and plan around it. They work with brokers who specialize in surety, not generalists who handle bonds as an afterthought. They keep their financials tight and current. They retain earnings instead of distributing everything at year end.

The SBA Surety Bond Guarantee Program is genuinely underused by small trade contractors. Roofing, masonry, and concrete firms that could qualify for public work through the SBA program never apply because they do not know it exists or assume they will not qualify. That assumption costs them real revenue.

Bonding is not a bureaucratic hurdle. It is a financial credibility signal. The contractors who understand that and build toward it consistently are the ones who grow from $2 million in annual revenue to $8 million without hitting a wall.

— Dave

Ready to get your bonding in order?

Bonding is one of the most misunderstood parts of running a trade business, and getting it wrong costs you bids. Subascent helps electrical, plumbing, HVAC, roofing, and other specialty trade contractors understand the bonding process, connect with the right surety brokers, and structure their financials to improve approval odds and capacity over time.

If you are ready to stop losing bonded work to contractors with better financial positioning, start with the Subascent bonding capacity guide built specifically for trade subs. You will find practical steps to improve your working capital, grow your bonding limit, and qualify for larger projects without guessing at what sureties want to see.

FAQ

What is a surety bond in simple terms?

A surety bond is a three-party financial guarantee where a surety company backs a contractor's promise to complete a project and pay subcontractors and suppliers. If the contractor fails, the surety pays the project owner and then seeks full reimbursement from the contractor.

How much does bonding cost for a small contractor?

Bond premiums run 1%–3% of the contract value for established contractors with good credit. On a $500,000 contract, that is $5,000 to $15,000. New or credit-challenged contractors pay 3% or more.

What is the SBA Surety Bond Guarantee Program?

The SBA Surety Bond Guarantee Program guarantees 80%–90% of surety losses on contracts up to $9 million, allowing sureties to approve small contractors they would otherwise decline. It is the primary path for new or higher-risk contractors to access bonded work.

How do I increase my bonding capacity over time?

Retain 50%–75% of net profits inside the business to grow working capital, since bonding capacity equals roughly 15–20 times working capital. Grow project sizes incrementally and maintain current, CPA-prepared financial statements.

Do I need a separate broker for bonding and insurance?

Yes. A surety-specific broker understands underwriting logic and advocates for better approval terms in ways a general insurance agent cannot. Submit bond applications separately from insurance renewals to avoid delays and entity name mismatches.