Equipment costing is the process of calculating the full ownership and operating cost of a machine, then expressing that cost as a rate applied to project bids and budgets. Most contractors who underprice jobs do not have a labor problem. They have an equipment problem. They charge what feels right instead of what the numbers require. Understanding how equipment costing works for contractors means separating ownership costs, operating costs, and overhead into a defensible hourly rate before a single bid goes out the door.

How does equipment costing work for contractors?

Equipment costing starts with one foundational truth: the purchase price is only 25–40% of total lifecycle costs. The remaining 60–75% comes from ongoing operating, maintenance, and end-of-life expenses. That means a $120,000 excavator will cost you somewhere between $180,000 and $360,000 over its working life. If your bid rates only reflect the purchase price, you are funding the rest out of your margin.

The industry term for this full calculation is the equipment cost recovery rate. It is the hourly rate a contractor must charge to a job just to break even on owning and running that machine. Specialty trade contractors in masonry, concrete, roofing, and framing all carry equipment on their books. Getting this rate wrong is one of the fastest ways to close a profitable-looking job at a loss.

Pro Tip: Build your equipment cost recovery rate in a spreadsheet before bidding season. Update it every january when insurance renewals and fuel contracts reset.

What are the core components of equipment costs?

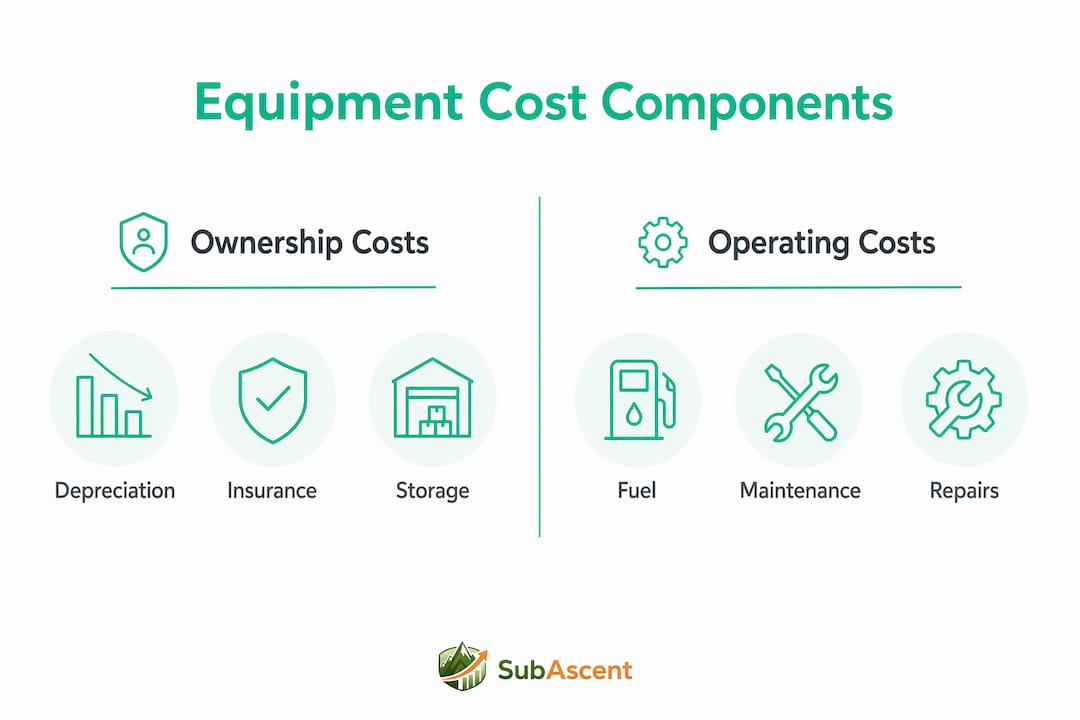

Equipment costs fall into three buckets: ownership costs, operating costs, and overhead allocation. Each one requires a different calculation method.

Ownership costs

Ownership costs are fixed. They accrue whether the machine runs or sits in your yard.

- Depreciation: Heavy equipment loses 20–40% of its value in the first years of ownership. Use economic depreciation in your job costing, not the IRS schedule. Tax depreciation accelerates write-offs for tax purposes but causes insufficient replacement funding when applied to job cost rates.

- Insurance: Annual premiums vary by machine type and coverage level.

- Interest or capital cost: Whether you financed the machine or paid cash, there is a cost of capital tied up in that asset.

- Taxes, licensing, and storage: Often overlooked but real. Storage alone can run several hundred dollars per month for larger equipment.

Ownership costs typically run $20,000–$50,000 annually per machine. That is the floor you must recover before you earn a dollar of profit on any job that uses it.

Operating costs

Operating costs vary with usage. They include fuel, repairs, routine maintenance, wear items like blades and teeth, and operator training. Maintenance alone consumes 2–5% of purchase price annually. On a $120,000 machine, that is $2,400–$6,000 per year just to keep it running. Operator training averaged $774 per employee, which is a real line item that most estimators forget entirely.

Calculating the hourly rate

The formula is straightforward:

- Add up all annual ownership costs (depreciation, insurance, interest, taxes, storage).

- Add annual operating costs (fuel, maintenance, repairs, wear items).

- Divide the total by expected usage hours for the year.

Example: $30,000 in annual fixed costs divided by 1,200 expected hours equals $25 per hour. That is your break-even ownership rate. Add operating costs per hour on top of that to get your full cost recovery rate.

How do usage hours affect your equipment hourly rate?

Utilization is the variable that most contractors ignore, and it is the one that destroys margins fastest. The math is unforgiving. If your annual fixed costs are $30,000 and you only use the machine 600 hours instead of 1,200, your hourly cost doubles to $50. You are still charging $25 on your bids. You are losing $25 every hour that machine runs.

Idle equipment is not free. It keeps accruing insurance, depreciation, and storage costs every day it sits. One contractor saved $85,000 annually by tracking and reducing idle equipment charges. That is not a rounding error. That is a full-time employee's salary recovered from better fleet management.

Pro Tip: Track equipment hours by job using telematics or even a simple paper log at the yard. If a machine sits idle for more than two weeks, assign it a standby cost code so the overhead shows up in your WIP report instead of disappearing.

| Scenario | Annual fixed costs | Usage hours | Hourly ownership cost |

|---|---|---|---|

| Full utilization | $30,000 | 1,200 | $25.00 |

| Half utilization | $30,000 | 600 | $50.00 |

| Low utilization | $30,000 | 300 | $100.00 |

The table makes the risk visible. A concrete or masonry contractor who bids a winter job assuming summer utilization rates will price that machine at half its true cost.

Break-even rates vs. market bid rates: which one should you use?

The answer is both, and you need to keep them separate. The USACE methodology separates owning costs from operating costs to establish a true baseline. That baseline is your break-even internal rate. It covers everything without profit. It is the floor below which you cannot go without losing money.

The market bid rate is what the rental market charges for a comparable machine, adjusted for your profit margin goal. Rental rates reflect supply, demand, and regional competition. They are not calculated from your actual costs. Setting your bid rates purely by market prices without knowing your internal break-even rate is how contractors underprice jobs and erode profit.

A two-tiered rate system works best for specialty trade contractors:

- Internal rate: Used for job costing, WIP reporting, and budget vs. actual tracking. Reflects true cost recovery.

- External bid rate: Used in proposals to GCs and owners. Reflects market rates plus your target margin.

The gap between the two is your equipment margin. If the market rate is $45/hour and your internal rate is $25/hour, you have $20/hour of margin to work with. If the market rate is $28/hour and your internal rate is $25/hour, you have almost no room for error on that job.

| Rate type | Purpose | Based on |

|---|---|---|

| Break-even internal rate | Job costing, WIP, budget tracking | Actual ownership and operating costs |

| Market bid rate | Client proposals, GC bids | Rental market pricing plus margin |

Separating these two rates is the single most clarifying thing a roofing or framing estimator can do for their bidding process. It turns equipment pricing from a gut call into a calculated decision.

How to integrate equipment costing into your job costing system

Equipment costs belong in your job costing system at the job level, not spread evenly across all work. Overhead smearing is the practice of allocating equipment costs as a flat percentage of revenue or labor. It distorts every profitability report you run. A job that used the excavator for 80 hours looks the same as one that used it for 8 hours. Your WIP is lying to you.

Here is how to fix it:

- Assign equipment cost codes to each job. Every machine gets a cost code. Every hour it runs on a job gets posted to that code.

- Separate fuel and operator costs from ownership recovery. Fuel is an operating cost. The operator's wages are a labor cost. The machine's depreciation and insurance are ownership costs. Mixing them into one line makes it impossible to diagnose where margin went.

- Review and update your equipment rates at least annually. Insurance renewals, fuel price shifts, and repair history all change your true cost. Rates set three years ago are probably wrong today. Many contractors tie this review to their annual job costing review at year-end close.

- Use your monthly close to catch drift. If a job's equipment costs are running 20% over budget at the halfway point, you need to know that in month two, not at final billing.

Tracking usage hours accurately is the foundation of all of this. Whether you use telematics, a field log, or a foreman timecard system, the data has to flow from the field to your cost system in real time.

Own or rent? A practical framework for specialty trade contractors

Ownership makes sense when you use a machine consistently across multiple jobs throughout the year. Renting makes sense when usage is project-specific, seasonal, or unpredictable.

Owning equipment:

- Fixed costs continue regardless of utilization

- Tax depreciation benefits available (but use economic depreciation for job costing)

- Capital tied up reduces working capital and can affect bonding capacity

- Repair and breakdown risk falls entirely on you. Breakdown downtime costs $500–$5,000 per day

- ASC 842 lease classification errors can distort financial reporting and bonding ratios if leases are misclassified

Renting equipment:

- Costs are predictable and project-specific

- Maintenance and repair risk transfers to the rental company

- No capital tied up, which protects bonding capacity

- Rental rates are typically higher per hour than owned equipment at full utilization

- No residual value or resale upside

The break-even point between owning and renting depends on your utilization rate. If you can run a machine at or above 60–70% of its available hours annually, ownership usually wins on cost. Below that threshold, renting is often cheaper when you factor in idle fixed costs.

Key takeaways

Accurate equipment costing requires calculating a break-even internal rate from true ownership and operating costs, then applying that rate by actual job usage to protect margin on every bid.

| Point | Details |

|---|---|

| Purchase price understates true cost | Ongoing costs represent 60–75% of total lifecycle expenses, not the purchase price. |

| Utilization drives hourly rate | Halving usage hours doubles your hourly ownership cost, directly eroding job margin. |

| Use two separate rates | Keep an internal break-even rate for job costing and a market bid rate for proposals. |

| Charge costs to jobs, not overhead | Assign equipment cost codes by job to prevent overhead smearing in WIP reports. |

| Review rates annually | Insurance, fuel, and repair costs shift yearly; outdated rates produce inaccurate bids. |

The number most contractors get wrong

Most estimators I talk to know their labor burden rate to the decimal. Ask them their equipment cost recovery rate and you get a shrug or a number pulled from a rental catalog. That gap is where margin disappears.

The mistake is not laziness. It is that equipment costs feel fixed and invisible. You bought the machine, you insure it, you maintain it. But because those costs do not show up on a weekly payroll run, they do not feel urgent. They are urgent. A machine sitting idle for two months while you wait for the next concrete pour is still burning $3,000–$5,000 in fixed costs per month.

The contractors who get this right do two things differently. First, they calculate an internal rate based on real numbers, not rental market prices. Second, they post equipment hours to jobs the same way they post labor hours. No exceptions. When the job closes, they know exactly what the machine cost on that project.

The technology to do this is not complicated. A spreadsheet handles the rate calculation. A job costing tool handles the allocation. What it takes is the discipline to build the rate, update it annually, and enforce the cost code discipline in the field. That discipline is worth more per year than most equipment purchases.

— Dave

Subascent makes equipment cost tracking part of every bid

Specialty trade contractors in masonry, concrete, roofing, and framing need job costing built around how they actually work, not how a general contractor's software assumes they work.

Subascent's bid and job software is built for specialty trade subs who need to track equipment costs, labor, and materials at the job level without rebuilding a spreadsheet for every bid. You can assign cost codes to equipment, track usage against budget, and catch margin drift before a job closes. If you are currently spreading equipment costs as overhead or guessing at hourly rates, Subascent gives you the structure to fix that without a six-month implementation. Explore the platform at subascent.com/shop.

FAQ

What is an equipment cost recovery rate?

An equipment cost recovery rate is the hourly rate a contractor must charge to a job to fully recover all ownership and operating costs for a machine. It is calculated by dividing total annual fixed and operating costs by expected usage hours.

Why does utilization affect equipment hourly cost so much?

Fixed ownership costs like depreciation and insurance do not change with usage. When a machine runs fewer hours, those fixed costs spread across fewer hours, which raises the cost per hour significantly.

Should contractors use IRS depreciation for job costing?

No. IRS tax depreciation accelerates write-offs for tax purposes but understates true replacement costs in job costing. Economic depreciation produces more accurate job cost rates and supports fleet renewal funding.

What is the difference between an internal rate and a market bid rate?

The internal rate covers your actual costs with no profit. The market bid rate reflects what the rental market charges, adjusted for your margin goal. Separating the two lets you price competitively while still tracking true job-level profitability.

When does renting equipment make more sense than owning?

Renting is typically more cost-effective when a machine will run below 60–70% utilization annually. Below that threshold, idle fixed costs on owned equipment often exceed the premium paid on rental rates.