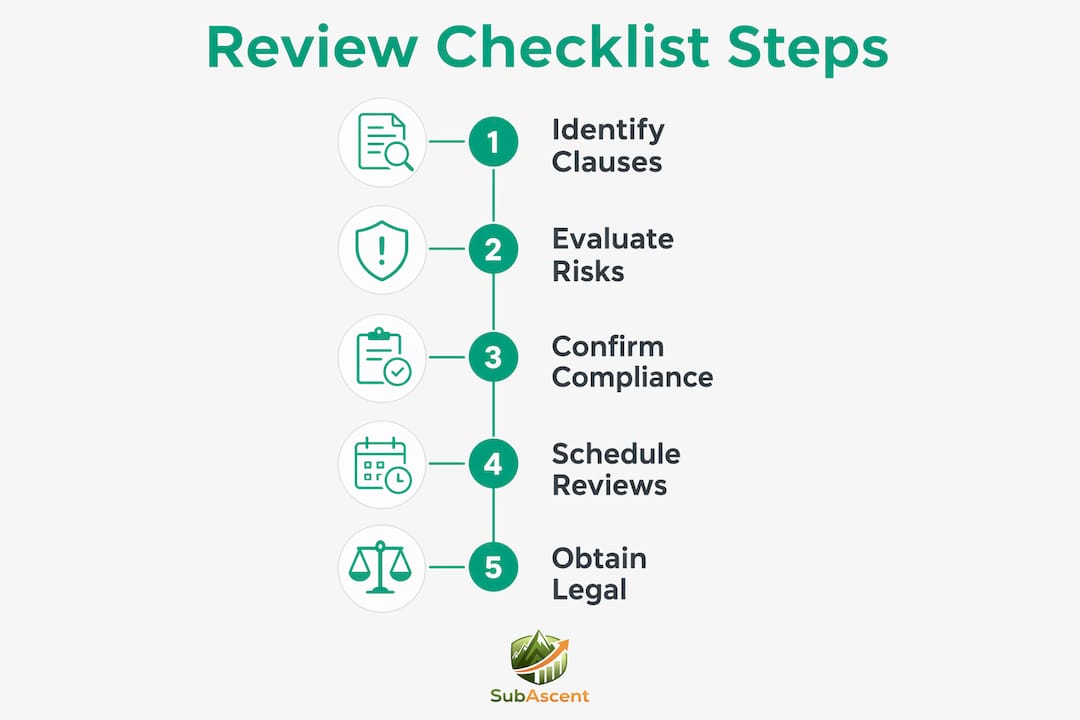

A subcontract agreement review checklist is a structured tool that specialty trade subcontractors use to systematically evaluate every contract clause before signing, protecting cash flow and limiting liability exposure. Without one, electrical, plumbing, HVAC, roofing, and masonry subs routinely sign agreements that shift unreasonable risk onto them. LazyQS identifies 12 core clause areas that consistently create financial exposure for specialty trades. The industry term for this process is contract risk review, and a well-built checklist for subcontract review turns that process from a legal exercise into a commercial one.

What key contract clauses must specialty trade subs review?

The contract review process starts with payment terms, and that is where most of the financial risk lives. Your checklist for subcontract review must confirm the payment interval, the mechanism for submitting applications, and the due dates for both payment notices and pay less notices. Under UK construction law, the Housing Grants Act enforces strict payment timelines, and missing a notice window can trigger an immediate payment obligation regardless of any valuation dispute. In the US, prompt payment statutes vary by state, but the same principle applies: vague due dates cost you money.

Beyond payment, a thorough subcontractor contract checklist covers these clause areas:

- Retention and release timing. Confirm the retention percentage, the trigger for release, and whether release is tied to practical completion of the main contract or your own work. Undefined release triggers are a common cash flow trap.

- Scope of work and referenced documents. Every exhibit, drawing set, and specification referenced in the contract must be listed and received. Missing scope exhibits cause disputes because subcontractors price work that was never formally included.

- Program and extension of time provisions. Check whether you have the right to claim additional time for GC-caused delays and what notice period is required to preserve that right.

- Liquidated damages (LDs). Identify the daily LD rate and calculate your maximum exposure. A $2,000-per-day LD clause on a 60-day delay is $120,000 of uncapped risk for a drywall or flooring sub.

- Insurance requirements. Verify that the required coverage types, limits, and endorsements are obtainable through your broker before signing. Insurance endorsements for Additional Insured status and Waiver of Subrogation must match the contract's required coverage periods and edition forms.

- Design liability. If you are a fire protection or low-voltage sub with design responsibilities, confirm the standard of care is "reasonable skill and care," not a fitness-for-purpose obligation, which is uninsurable under most professional indemnity policies.

- Indemnities and liability caps. Broad indemnities without caps can expose a $2M roofing sub to losses far exceeding the contract value. Push for mutual indemnities and a cap tied to contract value or insurance limits.

- Defects liability period. Confirm the duration and what obligations survive practical completion, particularly for HVAC or concrete subs where latent defects claims can surface years later.

- Termination rights. Check whether the GC can terminate for convenience and what payment you receive on termination. One-sided termination clauses with no payment for work in progress are a serious red flag.

- Dispute resolution. Confirm whether adjudication, arbitration, or litigation is specified, and check the notice periods required to preserve your right to claim.

Pro Tip: Read the flow-down clause carefully. If the subcontract incorporates the prime contract by reference, you may be bound by terms you have never seen. Request a copy of the prime contract before signing.

How to apply the subcontract agreement review checklist during contract evaluation

Sprintlaw recommends sequencing the review by commercial impact, starting with scope and payment before moving to liability and dispute clauses. That is the right call. Here is a practical sequence for estimators and project managers at specialty trade firms:

-

Build a document architecture map. List every document referenced in the subcontract: the agreement itself, scope exhibits, drawings, specifications, the prime contract, and any addenda. LegalClarity advises constructing this map before any clause-by-clause review so you understand the full document hierarchy. A concrete or masonry sub who skips this step often discovers mid-project that a spec section they never priced is contractually binding.

-

Reconcile exhibits against your bid. Pull your original estimate and compare it line by line against the scope exhibit in the contract. Confirm that every item you priced is included and that nothing new has been added. Verifying every referenced exhibit against bid assumptions prevents costly omissions that estimators only discover when the GC withholds payment.

-

Map payment dates to a calendar. Extract every date-driven obligation: application submission deadlines, payment due dates, pay less notice windows, and retention release triggers. Enter them into a shared calendar or project management tool immediately.

-

Assess insurance requirements against your current policy. Send the insurance section to your broker before you sign, not after. Confirm that Additional Insured endorsements, Waiver of Subrogation, and any umbrella requirements are achievable within your policy terms and budget.

-

Flag clauses that shift risk without compensation. Highlight any clause that requires you to absorb costs caused by others, including broad indemnities, pay-when-paid provisions without a reasonable time cap, and unilateral change order pricing rights.

-

Prioritize red flags for negotiation or legal review. Not every clause needs a lawyer. Focus legal review on indemnities, design liability, and LD exposure. Handle scope and payment terms internally using your checklist.

-

Create a contract compliance calendar. Once signed, diarize all payment and notice deadlines in a contract-specific diary. Minor timing errors on pay less notices have turned straightforward payment disputes into immediate payment obligations in court.

Pro Tip: Assign one person in your office to own the contract compliance calendar for each job. On a busy roofing or insulation project, missed notice deadlines are almost always a process failure, not a knowledge failure.

What are common red flags to watch for in subcontract reviews?

Certain contract features appear repeatedly in agreements that later generate disputes or cash flow problems. Knowing them in advance makes your subcontract agreement review faster and more targeted.

- Missing or vague payment due dates. If the contract does not state a specific due date for payment after application, you have no legal trigger for late payment claims. Push for a fixed number of days after application submission.

- Pay-when-paid clauses without a time cap. A pay-when-paid clause that contains no outside date can defer your payment indefinitely if the GC has a dispute with the owner. In many US states, these clauses are enforceable, which makes the time cap critical.

- Scope documents listed but not attached. Contracts that reference "Exhibit A" but do not attach it are a significant risk for framing, drywall, and glazing subs. Never sign until all exhibits are physically attached and reviewed.

- Overly broad indemnities. An indemnity that requires you to cover losses caused by the GC's own negligence is both commercially unfair and potentially uninsurable. This is one clause worth paying a construction attorney to redline.

- Undefined defects liability periods. A clause that ties your defects obligations to the main contract's defects period, without stating a maximum duration, can leave a fire protection or HVAC sub exposed for years beyond project completion.

- One-sided termination for convenience. If the GC can terminate at will but the payment on termination covers only work completed to date with no overhead or profit, you carry all the mobilization risk.

A subcontract that shifts every risk to the sub while offering no corresponding upside is not a contract. It is a liability transfer document. Read it that way and negotiate accordingly.

How do regional and jurisdictional requirements affect subcontract reviews?

Subcontract agreement guidelines are not uniform across the US, UK, or Australia. The legal regime in your project's jurisdiction directly affects which clauses carry the most risk and what default protections you have.

| Jurisdiction | Key Rule | Impact on Your Checklist |

|---|---|---|

| Texas | Notice of Contractual Retainage must be sent within 30 days of work completion to preserve lien rights | Add a retainage notice deadline to your compliance calendar on every Texas job |

| California | SB 61 and SB 440 cap retention at 5% on private work, with 2% interest penalties for late payment | Verify the retention percentage in your subcontract does not exceed the statutory cap |

| United Kingdom | Housing Grants Act requires payment notice within 5 days of due date and pay less notice at least 7 days before final payment date | Map every notice window to a calendar entry; non-compliance triggers automatic payment of the applied-for sum |

| Australia | Security of Payment legislation varies by state but generally provides adjudication rights for unpaid progress claims | Confirm your contract does not attempt to contract out of statutory payment rights |

Texas electrical and plumbing subs who miss the retainage notice deadline lose their lien rights on that money entirely. California masonry and concrete subs should check every new subcontract against the SB 61 retention cap before signing. In the UK, the VMA Services Ltd v Project One London Ltd case confirmed that non-compliant pay less notices expose GCs to "smash-and-grab" adjudications. That cuts both ways: if you are the sub, knowing this rule gives you leverage.

What tools and resources help manage the subcontract review process?

The right tools reduce the time your office spends on contract review without reducing the quality of that review.

- LazyQS. A UK-based contract review tool that flags risk clauses automatically across the 12 core areas identified in its subcontractor contract checklist. Useful for HVAC, fire protection, and low-voltage subs who review multiple subcontracts per month.

- A contract compliance calendar. A shared Google Calendar or project management tool with every payment and notice deadline entered at contract execution. This is the single highest-return habit a specialty trade PM can build.

- Your insurance broker. Treat your broker as part of the contract review team. Send them the insurance section before signing, not after. A good construction insurance broker will flag uninsurable requirements in 24 hours.

- A construction attorney on retainer. For indemnity clauses, design liability, and LD exposure above $50,000, a one-hour attorney review is cheaper than the risk. Many construction attorneys offer flat-fee contract review services.

- Subascent. For managing bids, tracking job status, and keeping contract documents organized across multiple active projects, Subascent's job and bid management platform gives specialty trade subs a single place to track what has been signed, what is pending, and what deadlines are coming up.

Understanding why cash flow matters for specialty trades makes it clear why contract review is not a back-office task. It is a revenue protection activity.

Key takeaways

A thorough subcontract agreement review checklist protects specialty trade subcontractors by identifying payment risks, scope gaps, and liability exposures before a contract is signed.

| Point | Details |

|---|---|

| Start with payment terms | Confirm due dates, notice windows, and pay-when-paid caps before reviewing any other clause. |

| Map all referenced documents | Every exhibit and flow-down document must be received and reconciled against your bid before signing. |

| Adapt for your jurisdiction | Texas retainage notices, California SB 61 retention caps, and UK Housing Grants Act timelines each require specific checklist items. |

| Verify insurance before signing | Send the insurance section to your broker at review stage, not after execution, to confirm endorsements are achievable. |

| Build a compliance calendar | Enter every payment and notice deadline into a shared calendar at contract execution to prevent costly timing errors. |

Why I treat every subcontract like a cash flow forecast

Most specialty trade owners hand a new subcontract to their office manager and say "check it over." That is not a review process. It is a hope strategy.

The contracts that have cost subs the most money in my experience are not the ones with aggressive LD clauses or broad indemnities. They are the ones where the scope exhibit was missing, the retention release was tied to the main contract's final account, and nobody noticed until the job was done and the money was stuck. A framing sub I know waited 14 months for retention release because the GC's prime contract had a defects period that nobody on the sub's side had ever read.

Sprintlaw's advice to sequence review by commercial impact is exactly right. Scope and payment first. Liability and disputes second. That sequencing forces you to think like a business owner, not a lawyer. The goal is not a perfect contract. The goal is a contract where you know exactly where the risk sits and you have priced or mitigated it accordingly.

Build the checklist once. Use it on every job. Assign one person to own the compliance calendar. Those three habits will do more for your cash flow than any contract negotiation tactic.

— Dave

How Subascent helps specialty trade subs manage contracts and bids

Running a thorough contract review on every subcontract is hard when your estimator is building three bids at once and your PM is chasing submittals. Subascent is built specifically for specialty trade subs, including electrical, plumbing, HVAC, roofing, and masonry businesses with 1 to 50 employees.

The platform keeps your bids, job documents, and contract records in one place, so nothing falls through the cracks between estimate and execution. When a new subcontract lands, your team has the bid assumptions right there to reconcile against the scope exhibit. Explore Subascent's subcontractor job and bid management software to see how it fits your trade. You can also check out the Subascent Chrome extension for faster bid and contract tracking directly from your browser.

FAQ

What is a subcontract agreement review checklist?

A subcontract agreement review checklist is a structured list of contract clauses and risk areas that specialty trade subcontractors evaluate before signing a subcontract. It covers payment terms, scope, retention, insurance, indemnities, and dispute resolution to identify financial and legal exposure.

How many clauses should a subcontract review cover?

A practical subcontract review covers at least 12 core clause areas, including payment terms, retention, set-off risks, scope, schedule, liquidated damages, insurance, design liability, indemnities, defects period, termination, and disputes.

What is the biggest risk in a subcontract agreement?

Payment terms and scope definition carry the highest financial risk for specialty trade subs. Vague payment due dates and missing scope exhibits are the two most common sources of disputes and cash flow problems on construction projects.

Do subcontract review requirements differ by state?

Yes. Texas requires a Notice of Contractual Retainage within 30 days of work completion to preserve lien rights. California caps retention at 5% on private work under SB 61 and SB 440. Every specialty trade sub should adapt their contract compliance checklist to the project's jurisdiction.

When should a specialty trade sub get legal review of a subcontract?

Get legal review on indemnity clauses, design liability provisions, and liquidated damages exposure above $50,000. For standard payment and scope terms, a well-built internal checklist and a conversation with your insurance broker is sufficient.