Bonding for subcontractors is a three-party financial guarantee between the subcontractor, the general contractor, and a surety company that ensures the subcontractor completes their work and pays their suppliers and laborers. If you run an electrical, HVAC, plumbing, or roofing trade business, you will encounter bonding requirements on virtually every commercial or public project you bid. Understanding what does bonding mean for subcontractors is not optional knowledge. It determines which jobs you can win, how much those jobs cost you to execute, and how much personal financial risk you carry when you sign a contract. This guide breaks down bond types, bonding requirements, costs, and the practical business implications every trade professional needs to know.

What does bonding mean for subcontractors?

A subcontractor performance bond is a legal contract that guarantees the subcontractor will complete their scope of work according to the subcontract terms. The bond involves three parties: the subcontractor (the principal), the general contractor (the obligee), and the surety company (the guarantor). If the subcontractor defaults, the surety steps in to cover the financial loss or arrange for project completion.

Bonding is not the same as insurance. With insurance, the insurer absorbs the loss. With a surety bond, the subcontractor remains fully liable. The surety pays the claim first, then pursues the subcontractor for full reimbursement. That distinction matters enormously when you are signing a personal indemnity agreement, which most sureties require.

The core purpose of bonding is risk transfer. The general contractor transfers the risk of subcontractor default to the surety company. The surety then prices that risk based on the subcontractor's financial strength, credit history, and project track record. For trade businesses in electrical, masonry, fire protection, or drywall, bonding is the financial credential that proves you can perform.

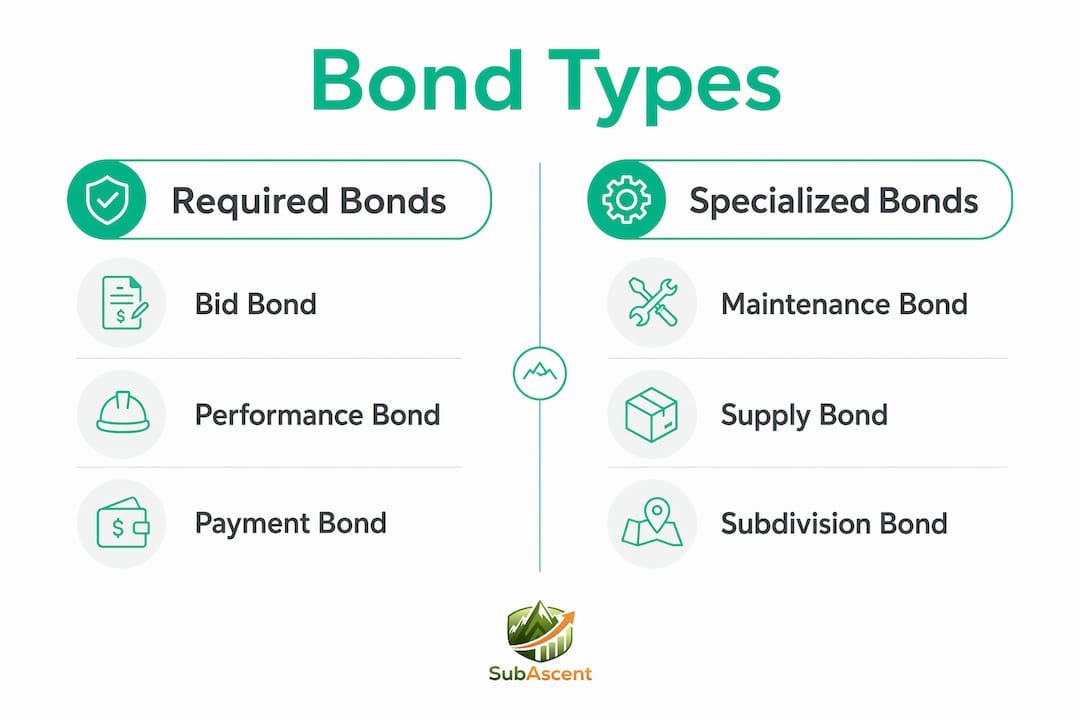

What types of bonds apply to subcontractors?

Three bond types appear most often in subcontractor agreements. Each serves a different function, and each protects a different party in the project chain.

- Performance Bond: This bond guarantees that the subcontractor will complete their scope of work. If the sub defaults, the surety covers the cost of completion or pays damages to the GC. A performance bond protects the GC from financial loss caused by subcontractor failure.

- Payment Bond: This bond guarantees that the subcontractor will pay their own suppliers, material vendors, and laborers. It protects lower-tier parties from non-payment. On federal projects, the Miller Act payment bond gives subcontractors a legal claim process if they go unpaid.

- Bid Bond: This bond accompanies a bid submission and proves the subcontractor has the financial backing to enter into the contract if awarded. If the sub wins the bid but refuses to sign the contract, the surety pays the GC the difference between the winning bid and the next lowest bid.

These three bonds often work together on the same project. A GC may require a bid bond during the tender phase, then require both a performance bond and a payment bond before issuing a notice to proceed.

Pro Tip: Always read the bid documents before pricing a job. Bond requirements buried in Division 00 of the spec book can add 1%–3% to your cost. Missing that line item kills your margin before the first crew shows up.

Specialized trades carry higher risk profiles on complex projects. Electrical and HVAC subcontractors are frequently required to be bonded because schedule delays or performance failures in those trades cascade across the entire project. GCs know this, and their sureties know it too.

Who decides bonding requirements for subcontractors?

Bonding requirements for subcontractors come from two sources: federal law and the general contractor's contract terms. Understanding which applies to your project tells you what documentation you need and when.

Federal Law: The Miller Act

The Miller Act requires prime contractors to post performance and payment bonds on federal construction projects over $150,000. The law does not directly require subcontractors to be bonded. However, GCs on federal projects routinely flow down bonding requirements to their subs, particularly on large or complex scopes.

General Contractor Requirements

Most bonding requirements subcontractors face are contractual, not statutory. The GC decides whether to require bonds based on contract value, project risk, and guidance from their own surety. GC sureties often recommend bonding back subcontractors on larger or complex projects as a risk management strategy. That recommendation from the GC's surety is often what triggers the bonding requirement in your subcontract, not an arbitrary GC decision.

Documentation Requirements by Project Size

Bonding applications scale with contract value. Here is what sureties typically require:

| Contract Value | Documentation Required |

|---|---|

| Under $750,000 | Simple bond application, basic financial info |

| $750,000 to $2,000,000 | Reviewed or compiled financial statements |

| Over $2,000,000 | CPA-audited financial statements |

These thresholds scale with contract value and reflect the surety's need to verify your financial capacity before guaranteeing your performance. If you are a framing or concrete sub growing into larger commercial work, getting your financials in order before you need a bond is the move. Waiting until a GC asks for a bond on a $3 million job is too late to start building a relationship with a CPA.

- Confirm bond requirements before submitting your bid.

- Contact your surety agent early to confirm your current bonding capacity.

- Gather financial statements, work-in-progress schedules, and bank references in advance.

- Factor the bond premium into your bid price before submission.

- Review the indemnity agreement with an attorney before signing.

How much does bonding cost subcontractors?

Bond premiums typically run 1%–3% of the total subcontract value. That range is wide because the surety prices each bond based on the subcontractor's specific risk profile.

Three factors drive your premium toward the low or high end of that range:

- Financial strength: Sureties look at your working capital, net worth, and debt levels. Strong balance sheets get better rates.

- Credit history: Personal and business credit scores matter. A low credit score signals risk to the surety and raises your premium.

- Project risk: Larger contracts, unfamiliar project types, or tight schedules push premiums higher.

Bonding capacity is tied to roughly 10–20 times a contractor's net working capital. A roofing sub with $200,000 in net working capital can typically bond projects up to $2,000,000–$4,000,000. That ceiling is a hard business constraint. Growing past it requires building your balance sheet, not just winning more work.

Most subcontractors pass bond costs through in their bids. If the GC requires a bond, the premium is a legitimate project cost. Include it as a line item in your estimate the same way you include material costs or equipment rental. Absorbing it silently destroys your margin.

Pro Tip: Ask your surety agent for a bond cost estimate before you finalize your bid. A quick call takes five minutes and prevents you from eating a $15,000 premium on a $500,000 electrical contract.

What are the practical implications of bonding for your business?

Bonding affects more than just individual projects. It shapes your business's growth trajectory, your relationships with GCs, and your personal financial exposure.

- Project eligibility: Many public and commercial projects require bonded subs. Without bonding capacity, you cannot bid those jobs. Bonding capacity controls which projects subcontractors can pursue, which makes financial discipline a direct revenue driver.

- Personal liability: Surety bonds are not a shield. Sureties require full reimbursement for any claims paid, often under personal indemnity agreements that put your personal assets at risk. Signing a bond is a serious financial commitment.

- Surety relationships: Your surety agent is a long-term business partner, not a one-time vendor. Sureties that trust your financials and track record will increase your capacity over time. Sureties that see late filings, thin margins, or project losses will tighten your limits or decline to bond you.

- Negotiation leverage: Understanding why a GC requires a bond gives you room to negotiate. If the requirement comes from the GC's surety rather than the project owner, there may be flexibility on bond amount or type, especially for lower-risk scopes.

"Bonding is the financial credential that separates subcontractors who can grow into larger commercial work from those who stay stuck in the same project tier indefinitely."

Tracking your subcontract trade bidding opportunities alongside your bonding capacity is a discipline that pays off. If your capacity is $3 million and you have $2.5 million in bonded work in progress, you have limited room to take on another bonded project without growing your working capital first. That is a planning problem, not just a finance problem.

Maintaining clean, current financials is the single most effective way to grow your bonding capacity. A subcontractor financial dashboard that tracks job profitability, cash position, and accounts receivable gives your surety the confidence to extend more capacity. Sureties want to see that you know your numbers.

Key takeaways

Subcontractor bonding is a three-party financial guarantee that controls project eligibility, personal liability, and business growth capacity for every trade professional in commercial construction.

| Point | Details |

|---|---|

| Bonding is a guarantee, not insurance | You remain fully liable to the surety for any claims paid, often under personal indemnity. |

| Three bond types apply to subs | Performance, payment, and bid bonds each protect different parties in the project chain. |

| GCs set most bonding requirements | Federal law covers prime contractors; subcontractor bonding is usually a contractual GC decision. |

| Premiums run 1%–3% of contract value | Pass the cost through in your bid as a line item, not as an absorbed expense. |

| Bonding capacity limits your growth | Capacity is tied to net working capital, so strong financials directly expand your project ceiling. |

The part most trade owners miss about bonding

Most trade owners I talk to treat bonding as a compliance checkbox. They get the bond because the GC requires it, they pay the premium, and they move on. That mindset costs them money and opportunity.

The first thing most people get wrong is confusing bonds with insurance. Insurance absorbs your loss. A bond does not. When a surety pays a claim on your behalf, they come back for every dollar, plus costs. I have seen electrical and HVAC subs sign personal indemnity agreements without reading them carefully, then face personal asset exposure when a project went sideways. Read the indemnity agreement. Every word.

The second mistake is treating bonding capacity as a fixed ceiling. It is not. It is a function of your balance sheet. Subs who invest in clean CPA-reviewed financials, maintain strong cash positions, and communicate proactively with their surety agent consistently grow their capacity faster than subs who treat their books as an afterthought. Your surety agent is one of the most valuable relationships in your business. Call them before you need a bond, not the day the GC asks for one.

The third thing worth saying: bonding is a competitive advantage if you use it that way. A masonry or concrete sub that can bond a $5 million project competes in a different market than one that cannot. The subs who understand this build their financials deliberately, not just to satisfy their accountant, but to unlock the next tier of work.

— Dave

How Subascent helps you stay ahead of bonding requirements

Bonding documentation, bid tracking, and contract management all create paperwork that piles up fast. Subascent is built specifically for specialty trade subcontractors, including electrical, plumbing, HVAC, roofing, and fire protection businesses, to manage bids, jobs, and the documentation that GCs and sureties require. When a GC asks for your work-in-progress schedule or your current bonded backlog, you need that information ready in minutes, not days. Subascent keeps your project data organized so you can respond fast and win more bonded work. Explore Subascent for subcontractor management and see how it fits your trade business.

FAQ

What does bonding mean for a subcontractor?

Bonding means a subcontractor has a surety-backed financial guarantee that they will complete their work and pay their suppliers. The bond is a three-party agreement between the subcontractor, the general contractor, and the surety company.

Is bonding required for all subcontractors?

No. The Miller Act requires bonds from prime contractors on federal projects over $150,000, but subcontractor bonding is determined by the general contractor's contract terms, not federal law in most cases.

How is a surety bond different from insurance?

A surety bond is a guarantee, not a transfer of loss. Unlike insurance, the subcontractor remains fully liable to the surety for any claims paid, often under a personal indemnity agreement. Read more about the differences in this subcontractor default insurance guide.

How much does a subcontractor bond cost?

Bond premiums typically run 1%–3% of the subcontract value, depending on the subcontractor's financial strength, credit history, and project risk. Most subcontractors include the premium as a line item in their bid.

What can a subcontractor do to increase their bonding capacity?

Maintain strong, CPA-reviewed financials, grow your net working capital, and build a consistent track record with your surety agent. Bonding capacity is typically limited to 10–20 times net working capital, so a stronger balance sheet directly raises your ceiling.