A bid bond is a financial guarantee that a contractor will honor their bid, sign the contract if awarded, and provide any required follow-up bonds. Every electrical, plumbing, HVAC, masonry, and roofing sub bidding public or private work needs to understand this instrument. The bid bond definition covers three parties: the principal (you, the contractor), the obligee (the project owner), and the surety company backing the guarantee. Get this wrong and you are not just losing a job. You are on the hook financially.

What is a bid bond and how does it protect the project owner?

A bid bond is a surety instrument, not an insurance policy. The distinction matters more than most trade contractors realize. Bid bonds represent credit, not insurance, which means the surety pays a claim on your behalf and then comes back to collect every dollar from you.

The bond protects the project owner from a specific risk: you win the bid, then walk away. Without a bid bond, an owner who selected the lowest bidder has no recourse if that contractor refuses to sign. They must rebid the project, absorb delays, and pay whatever the next contractor charges. A bid bond eliminates that exposure.

Penal sums typically range from 5% to 20% of the bid amount. Standard commercial projects sit at 5–10%. Federal contracts often require 20%. That percentage caps the surety's liability, not your liability as the contractor.

Bid bonds are standard on public projects and increasingly common on private commercial work. If you are a fire protection or low-voltage sub bidding school districts, hospitals, or government facilities, you will encounter bid bond requirements on nearly every invitation to bid.

How does a bid bond work step by step?

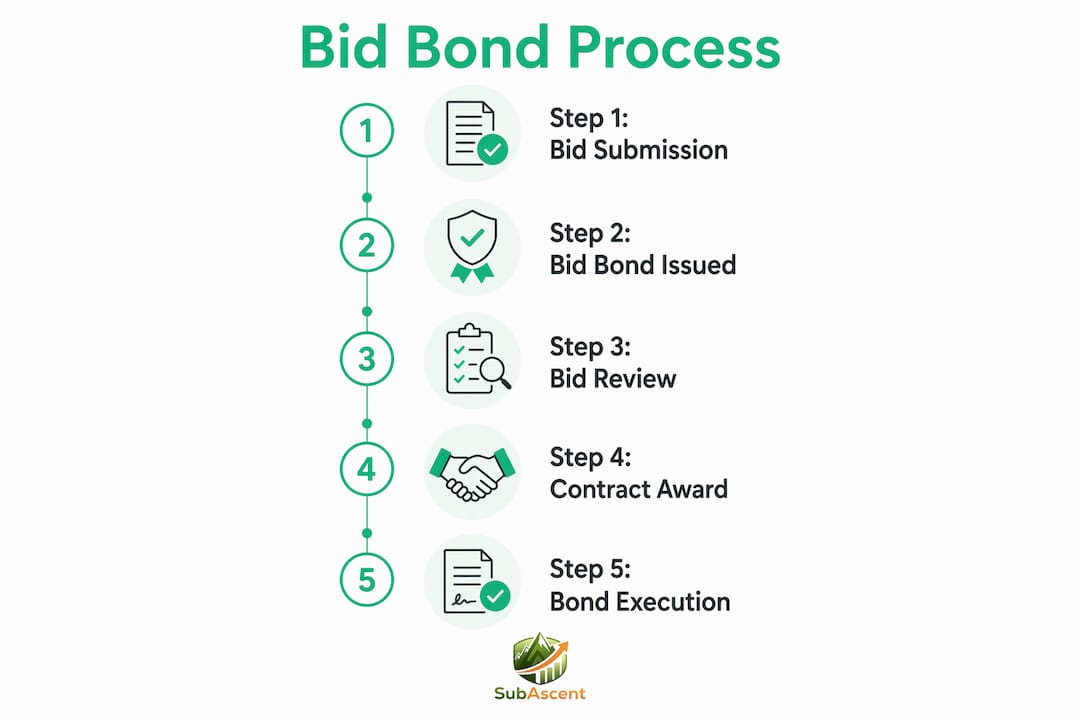

The lifecycle of a bid bond follows a predictable sequence. Understanding each stage helps you avoid costly mistakes.

- Bid submission. You submit your bid proposal along with the bid bond. The bond is typically a standard form provided by the surety or the project owner.

- Surety underwriting. Before issuing the bond, the surety reviews your credit history, financial statements, and work experience. This is not a formality. It is a genuine assessment of your financial health.

- Bid evaluation. The project owner reviews all submitted bids. Your bid bond is held during this period.

- Award and contract signing. If you win, you are expected to sign the contract and provide any required performance and payment bonds within the specified timeframe.

- Bond release. Once you sign the contract and deliver follow-up bonds, the bid bond is released and has no further effect.

- Default scenario. If you refuse to sign or cannot provide follow-up bonds, the owner files a claim. The surety pays damages equal to the difference between your bid and the next lowest bid, up to the penal sum.

The bid validity period governs how long the owner has to award the contract. Contractors must track bid validity closely to avoid being bound indefinitely or released unintentionally. Most bid validity windows run 30–90 days.

Pro Tip: Mark the bid validity expiration date in your calendar the moment you submit. If the award decision drags past that date, confirm in writing whether your bond obligation has been extended or released.

What are the costs and requirements for getting a bid bond?

Most specialty trade subs are surprised to learn that bid bonds carry no direct upfront fee in most cases. The surety does not charge a premium for a bid bond the way they do for a performance bond. What they do require is a thorough look at your business.

The surety's underwriting process typically examines:

- Credit history. Personal and business credit scores for the owner and the company.

- Financial statements. Reviewed or compiled statements showing assets, liabilities, and working capital.

- Work history. Completed projects, project sizes, and trade experience relevant to the bid.

- Current workload. How much work you already have under contract and whether you have capacity.

- Bonding capacity. The maximum dollar value of work the surety will bond for you at any given time.

Your bonding capacity is the number that matters most. It signals to general contractors and owners how much financial weight your business can carry. A drywall or framing sub with a $5 million bonding capacity is a different conversation than one with $500,000.

Improving your bonding capacity takes time, but the steps are concrete. Subascent's guide on improving bonding capacity covers the specific financial moves that move the needle with sureties.

Pro Tip: Treat the surety underwriting process like a bank loan application. Clean financials, a strong balance sheet, and documented project history will get you better terms and higher capacity.

What are the legal risks of defaulting on a bid bond?

Defaulting on a bid bond is not a minor administrative issue. The financial and reputational consequences are serious and lasting.

Here is what happens when a contractor defaults:

- The owner files a claim. The obligee notifies the surety that you have failed to honor the bid.

- The surety investigates. The surety verifies the claim and calculates damages owed.

- The surety pays the owner. Payment covers the gap between your bid and the next lowest bid, capped at the penal sum.

- The surety pursues you. Under the indemnity agreement you signed, the surety recovers all payments plus legal fees directly from you.

- Your bonding access is damaged. A default on record makes future bonding harder and more expensive to obtain.

The indemnity agreement is the part most contractors underestimate. You are not just risking the penal sum. You are personally liable for every dollar the surety pays out, plus their investigation costs and legal expenses.

A bid bond default does not end with the surety absorbing the loss. It ends with the surety collecting from the contractor. Every dollar paid to the owner comes back as a debt you owe.

Bid bonds also protect owners from speculative low-ball bids. A concrete or steel sub who submits an unrealistically low number to win work, then walks away, creates real project delays and cost overruns for the owner. The bid bond is the mechanism that makes that behavior financially painful.

Understanding your default insurance options alongside bid bonds gives you a fuller picture of how risk is allocated across a project.

Bid bond vs performance bond: what is the difference?

These two bond types are frequently confused, but they serve completely different functions at different stages of a project.

| Feature | Bid bond | Performance bond |

|---|---|---|

| When it applies | During the bidding phase | After contract award |

| What it guarantees | You will sign the contract and provide follow-up bonds | You will complete the contracted work |

| Who it protects | Project owner during bid evaluation | Project owner during project execution |

| Trigger event | Contractor refuses to sign or provide bonds | Contractor fails to complete the work |

| Typical cost | No direct fee (credit-based) | Premium paid, typically 1–3% of contract value |

| Duration | Expires at contract signing | Runs through project completion |

Performance bonds guarantee contract completion after award, while bid bonds assure the owner that the winning bidder will actually show up to sign. A roofing or glazing sub needs to understand both because winning a bonded project requires you to convert the bid bond into a performance bond at award.

The practical implication for estimators: factor the performance bond premium into your bid. Bid bonds cost nothing upfront, but performance bonds carry a real premium that eats into margin if you forget to include it.

How specialty trade subs can use bid bonds strategically

Bid bonds are not just a compliance checkbox. Used well, they are a competitive tool.

Consistent ability to provide bid bonds signals financial stability and project capacity to general contractors. A GC evaluating three HVAC or insulation subs will weight bonding capability heavily, especially on larger jobs. If you can bond and your competitor cannot, you have already differentiated yourself before the numbers are even reviewed.

Practical ways to use bid bonds as a strategic asset:

- Maintain your bonding capacity year-round. Do not let your financials slip during slow periods. Sureties check current workload and balance sheet health every time you request a bond.

- Track bid validity dates without fail. Missing a validity window can expose you to unintended obligations or cost you the award entirely.

- Include bond requirements in your bid checklist. Every bid invitation should be reviewed for bond type, penal sum percentage, and submission format before you start estimating.

- Use your bonding history as a selling point. When talking to new GCs, mention your bonding capacity and clean surety record. It is a credibility signal that most subs never think to use.

Pro Tip: Before you start estimating a bonded project, confirm the required penal sum and whether a performance bond will be required at award. Build the performance bond premium into your number from day one.

Key takeaways

A bid bond is a credit instrument that binds you legally and financially the moment you submit it. Treat it that way from the first line of your estimate.

| Point | Details |

|---|---|

| Bid bonds are credit, not insurance | You reimburse the surety for every dollar paid in a claim, plus legal costs. |

| Penal sums range from 5% to 20% | Federal projects often require 20%; standard commercial work sits at 5–10%. |

| No upfront fee, but underwriting is real | Sureties review credit, financials, and work history before issuing any bond. |

| Default consequences are severe | A claim damages your bonding capacity and triggers personal liability under the indemnity agreement. |

| Bid bonds differ from performance bonds | Bid bonds cover the signing phase; performance bonds cover project execution. |

The part most trade subs get wrong about bid bonds

I have talked to a lot of electrical and plumbing owners who treat bid bonds as paperwork. Something you get from your surety agent, attach to the bid, and forget about. That mindset is expensive.

The indemnity agreement you sign when you get a bid bond is a personal guarantee. If you walk away from a winning bid because your numbers were wrong or your crew is overloaded, the surety pays the owner and then comes after you. Not your LLC. You. That is the part that does not show up in the one-page explainer your agent hands you.

The other thing I see constantly: subs who do not track bid validity periods. You submit a bond, the GC takes 75 days to make a decision, and suddenly you are not sure if you are still bound or not. That uncertainty is avoidable. Build bid validity tracking into your process the same way you track submittal deadlines.

The subs who use bonding well treat their surety relationship like a banking relationship. They keep their financials clean, they communicate with their agent before capacity issues arise, and they use their bonding record as a selling point with GCs. That approach turns a compliance requirement into a genuine competitive edge. If you are just getting started with bonded work, Subascent's guide on subcontract trade bidding is worth reading alongside this one.

— Dave

Manage your bids and bonds without the spreadsheet chaos

Tracking bid validity dates, bond requirements, and award deadlines across a dozen active bids is where things fall through the cracks. A missed validity window or a forgotten bond requirement on a federal project can cost you the award or trigger a claim.

Subascent is built specifically for specialty trade subs managing the full bid lifecycle, from invitation to award. The platform helps electrical, HVAC, roofing, and other trade contractors track bond requirements, bid deadlines, and contract status in one place, without rebuilding a spreadsheet every month. If you are bidding bonded work and managing it manually, see how Subascent works and find out what you are missing.

FAQ

What is the bid bond definition in simple terms?

A bid bond is a financial guarantee that a contractor will sign the contract and provide required bonds if they win a bid. It protects the project owner from financial loss if the winning bidder walks away.

How does a bid bond work when a contractor defaults?

The project owner files a claim with the surety. The surety pays the difference between the defaulting bid and the next lowest bid, up to the penal sum. The contractor then owes the surety that full amount plus any legal costs.

Why do I need a bid bond as a specialty trade sub?

Most public projects and many private commercial projects require bid bonds as a condition of bidding. Beyond compliance, a bid bond signals to general contractors that you have the financial capacity to perform the work.

What are the requirements for a bid bond?

Sureties require a review of your credit history, financial statements, completed project history, and current workload. There is typically no upfront fee, but you must qualify through the surety's underwriting process.

What is the difference between a bid bond and a performance bond?

A bid bond guarantees you will sign the contract after winning a bid. A performance bond guarantees you will complete the contracted work. Bid bonds apply during the bidding phase; performance bonds apply after contract award and run through project completion.